BY Tashiana Briggs, Partner – Tax, Healthcare and Professional Services, Adam Portacci, Director – Financial Advisory Health Care Valuation Services, and Josh Finrock, Director – Transfer Pricing, Weaver

BY Tashiana Briggs, Partner – Tax, Healthcare and Professional Services, Adam Portacci, Director – Financial Advisory Health Care Valuation Services, and Josh Finrock, Director – Transfer Pricing, Weaver

It appears the Grinch has stolen some of the jolly from the practice of medicine, with physicians facing a brutal reality: ever increasing clinical volume paired with declining margins. As a result, many practices are looking for ways to reduce cash outlays or show healthy income when seeking outside investment, particularly when operating a growing practice solely through a traditional professional corporation (PC) or PLLC structure. Fortunately, this season may present an opportunity to structure your medical practice in a way that  helps retain more cash within the business.

helps retain more cash within the business.

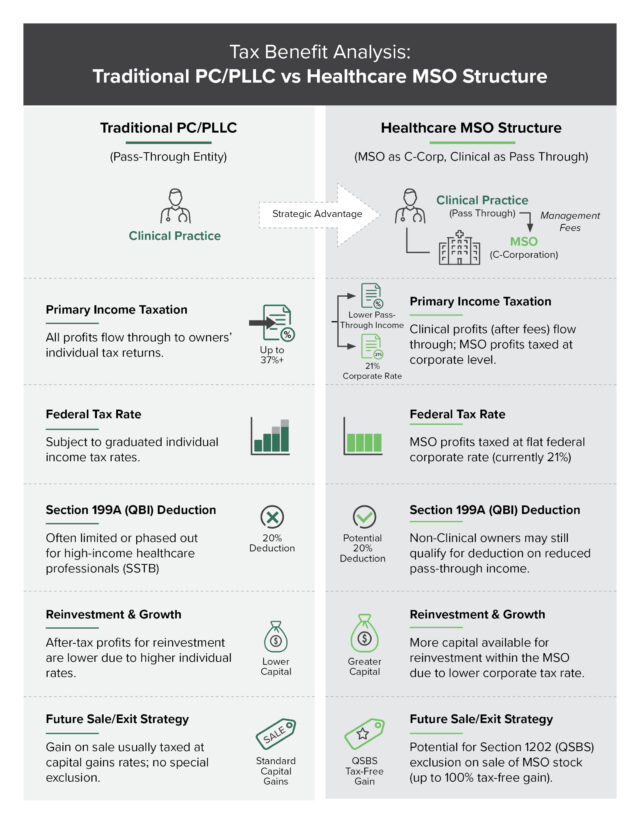

To address some of the challenges resulting from the corporate practice of medicine (CPOM) laws, equity interests have established the “friendly” PC structure. This structure aligns with CPOM laws while allowing physician-owned health care organizations to establish separate clinical and nonclinical operations of the business. By separating the clinical and nonclinical operations, physician-owned health care organization can seek venture capital and private equity funding.

The structure typically involves two entities: a PC, owned by licensed medical professionals, providing clinical or medical services  regulated under CPOM laws and a management services organization (MSO), not regulated to be owned by licensed medical professionals, providing services legally considered nonclinical.

regulated under CPOM laws and a management services organization (MSO), not regulated to be owned by licensed medical professionals, providing services legally considered nonclinical.

The operational benefits of an MSO — centralizing billing, HR and IT — are well known. But for astute practice owners, the MSO is not just an administrative convenience; it is a critical financial strategy designed to optimize after-tax cash flow.

The following is an overview of specific tax advantages available to MSOs.

Tax Structuring and Eligibility Considerations

The way an MSO is structured from a tax perspective has significant implications for its owners and the affiliated medical practices.

- Entity choice:

- C-Corporation: Can offer liability protection and potentially lower initial tax rates on retained earnings but faces double taxation on dividends and asset sales.

- S-Corporation: Allows profits and losses to be passed through directly to the owners’ personal income without being subject to corporate tax rates, avoiding double taxation. However, subject to certain limitations on ownership and classes of stock and reasonable compensation considerations

- Partnership/LLC (taxed as partnership): Provides flexibility in profit and loss allocation and pass-through taxation. This is often a preferred entity choice for MSOs with multiple owners.

- Common control rules: The “common control” rules under IRC Sections 414(b), (c), (m) and (o) are critical. If an MSO and its affiliated medical practices are considered a “controlled group,” they may be treated as a single employer for certain employee benefit plan purposes, impacting pension plans, profit-sharing plans and other benefits. This can also affect limitations on tax benefits and credit calculations. Careful structuring is needed to determine ownership percentages and operational control to avoid unintended aggregation. This is mostly seen between entities owned by the same doctor group.

- Gross receipts test and accounting methods: The gross receipts test (often tied to IRC Section 448) determines whether an entity can use the cash method of accounting. Businesses with average annual gross receipts of $32 million or less (2026 threshold, indexed for inflation) over the prior three taxable years can use the cash method. This simplifies accounting by recognizing income when received and expenses when paid, rather than when earned or incurred. MSOs and their related practices must carefully monitor aggregate gross receipts to ensure compliance if they wish to utilize the cash method. Staying under the gross receipts test threshold allows the use of the cash method of accounting and exempts you from many the deeper compliance headaches mentioned below. However, structures meeting the “common control” rules under IRC Section 414 (and other sections) mentioned above must be mindful of the aggregation rules requiring the gross receipts of multiple taxpayers to be combined.

Operational Tax Considerations

How you operate the MSO daily triggers specific code sections that impact your bottom line.

How you operate the MSO daily triggers specific code sections that impact your bottom line.

- Section 163(j) (limitation on business interest expense): Section 163(j) generally limits the deduction for business interest expense to 30% of adjusted taxable income (ATI). This can impact your MSO strategy if it involves leveraging debt to acquire real estate, expensive medical equipment or technology platforms. Smaller businesses that meet the gross receipts test (same threshold as for cash method eligibility) are generally exempt from this limitation. Therefore, remaining under the gross receipts threshold can provide both the benefit of using the cash method of accounting and exemption from the Section 163(j) interest limitation.

- Section 199A (qualified business income deduction): Section 199A allows eligible owners of pass-through entities (S-corporations, partnerships, sole proprietorships) to deduct up to 20% of their qualified business income (QBI). The interplay between the MSO, common control rules and Section 199A should be discussion point for maximizing the QBI deduction. A standalone medical practice often loses this deduction entirely as the deduction is subject to limitations for “specified service trades or businesses” (SSTBs), which includes the field of health. However, the QBI of a properly structured MSO providing purely administrative and back-office support with real substance and distinct operations could be eligible for the deduction and not subject to same limitations as the SSTB. If careful consideration is not given to the structuring of the MSO, the entire group could be considered as artificial separated and deemed an SSTB.

- Section 1202 (qualified small business stock exemption): Section 1202 provides a significant tax benefit: a tiered exclusion from gross income for a certain percentage (up to 100%) of gain from the sale of “qualified small business stock” (QSBS) held for more than three years, up to $15 million or 10x basis (whichever is greater). This exclusion cap begins being adjusted annually for inflation starting in tax year 2026.

- Eligibility: Spoiler alert, the Grinch strikes again. The issuing corporation must be a C-corporation (at the time of issuance and substantially all of its assets must be used in a qualified trade or business). Both the shareholders and the corporation must meet certain requirements including gross asset limitations.

- Health care MSOs and QSBS: For a health care MSO structured as a C-corporation, Section 1202 can be an incredibly attractive exit strategy for investors or founders (but requires selling shares). If the MSO’s activities do not primarily involve the performance of services in the field of health (i.e., it is not an SSTB), it could qualify as a QSBS. This reinforces the importance of the MSO’s operational scope and legal definition to maximize potential capital gains exclusions.

- State and local tax (SALT): State and local tax considerations must not be ignored as they often introduce the greatest complexity and risk, especially for MSOs operating across multiple state lines. If your MSO provides remote billing, IT support or telemedicine platform management to clinics spanning multiple states, you are creating “nexus” in those states. You may be subject to income tax, gross receipts taxes and sales tax on services in jurisdictions despite having no physical footprint. A sophisticated MSO structure must include a SALT analysis to ensure you do not trade federal savings for state-level liabilities.

Documentation Considerations

The MSO structure’s tax benefits are significant but attract intense IRS scrutiny. The separation (bifurcation) of clinical and nonclinical activities must be defensible. This is non-negotiable. Your compliance hinges entirely on robust, preemptive documentation, specifically requiring up-to-date fair market valuation (FMV) and transfer pricing reports to justify every management fee and transaction. Operating without this documentation is simply inviting risk that could be catastrophic.

CPOM Laws

The management fee paid by the PC to the MSO must be set at fair market value (FMV) to comply with CPOM laws and related fee-splitting prohibitions. Key reasons FMV is required under CPOM are:

- Avoids fee-splitting: Arbitrary or inflated fees tied to PC revenue could be interpreted as splitting professional fees with unlicensed parties, a direct CPOM violation in many states.

- Prevents undue control: FMV fees — set in advance via third-party valuations — demonstrate that the MSO’s role is strictly supportive, not controlling, thereby maintaining the PC’s clinical autonomy.

- Mitigates risks: Non-FMV fees risk regulatory scrutiny, leading to penalties, litigation or further enforcement actions.

Fixed fees (i.e., a set monthly amount) are often preferred for CPOM compliance but face operational and regulatory hurdles in ongoing arrangements. As the PC grows or service needs change, the fixed fee may not adjust automatically, leading to misalignment with actual costs or value provided. Without periodic reassessments (i.e., third-party valuations), the fee could drift from FMV over time, potentially violating CPOM by implying undue MSO control or inadequate compensation for services.

Percentage fees (i.e., a share of PC revenue) offer scalability but may bring more risk of conflict with CPOM or fee-splitting laws depending on the state. Moreover, percentage fees should also be regularly reevaluated for FMV to ensure compliance.

FMV discount or “scrape” mechanisms (i.e., adjusting fees downward or “scraping” excess payments back to ensure FMV alignment) are used in some arrangements, often via predetermined variable fees or clawbacks. These involve periodic valuations to calculate adjustments, which may be administratively burdensome. States may also view these as workarounds for prohibited structures, potentially leading to challenges in audits or enforcement.

Transfer Pricing

An MSO’s transactions with an affiliated or “friendly” PC, in which there is likely common control, are subject to transfer pricing rules and determined in accordance with Internal Revenue Code Section 482 (IRC 482).

If two organizations are under any type of common control and have transactions between them, the organizations are subject to IRC 482 from which the arm’s length standard is based. The arm’s length standard refers to organizations acting as independent parties would act under similar conditions. IRC 482 gives the IRS the ability to adjust revenue, expenses, credits or allowances to prevent the evasion of taxes and to reflect the true income of an organization.

The contract(s) or intercompany agreement between the MSO and PC should clearly define the assets leased, services provided, risks assumed and how the MSO fees are determined. Appropriate transfer pricing analysis documents functions, assets and risks while selecting the best method for establishing arm’s length pricing for the MSO fees. Any income at the PC is subject both to a corporate level of taxation and a shareholder level of taxation, putting pressure on the new ownership to manage the profit of the PC through the MSO fees. Where a group does not have proper support for the arm’s length nature of its MSO fees, the IRS may challenge aspects of MSO fees or challenge the value of the MSO fees and subsequently the deductibility for purposes of corporate level taxation. A PC generating losses or consistently generating zero income at the corporate level may indicate MSO fees that would not hold up under IRS scrutiny.

To structure an MSO and PC relationship appropriately, investors should consider the structure and methods of establishing arm’s length pricing for their MSO fees to align both with CPOM and IRC 482. By conducting a transfer pricing analysis, the PC ensures that services provided, risks assumed, contractual terms and economic conditions are considered when selecting the best method for establishing the arm’s length value of MSO fees. Typically, an MSO fees are established as either a fixed charge for services rendered based on value or a cost of performance plus a reasonable profit markup. While MSO and PC arrangements must align with IRC 482, they must prioritize legal considerations governing the separation of the MSO and the PC’s legal independence to make clinical decisions. In the case of IRS scrutiny, health care groups with MSO and PC arrangements need to manage potential risk of double taxation from adjustments to income or deductions, risk of transfer pricing penalties and risks related to compliance with CPOM laws.

Final Thoughts

The health care MSO structure offers a powerful framework for optimizing both the operational efficiency and tax position of health care providers. By carefully considering entity choice, navigating common control rules and strategically applying provisions like Sections 163(j), 199A and 1202, MSO owners can unlock significant tax benefits. However, the complexities of these rules necessitate meticulous planning and expert advice from legal and tax professionals to ensure compliance and maximize advantages.